A retail account is a personal brokerage account funded with the trader’s own money. A prop firm account is conditional access to a firm-controlled trading programme. Retail trading gives more ownership and withdrawal control, but the trader directly bears personal market losses. Prop firm trading can reduce the need to deposit large capital, but it adds rule risk, payout review, profit split, account-access risk and firm-specific restrictions.

Prop Firm Account vs Retail Account: The Direct Answer

This article is the prop-vs-retail account child guide inside the What Is Prop Trading? Hub. Use the Hub for the full prop trading model, then use this page to compare ownership, rules, payout control, risk burden and strategy fit.

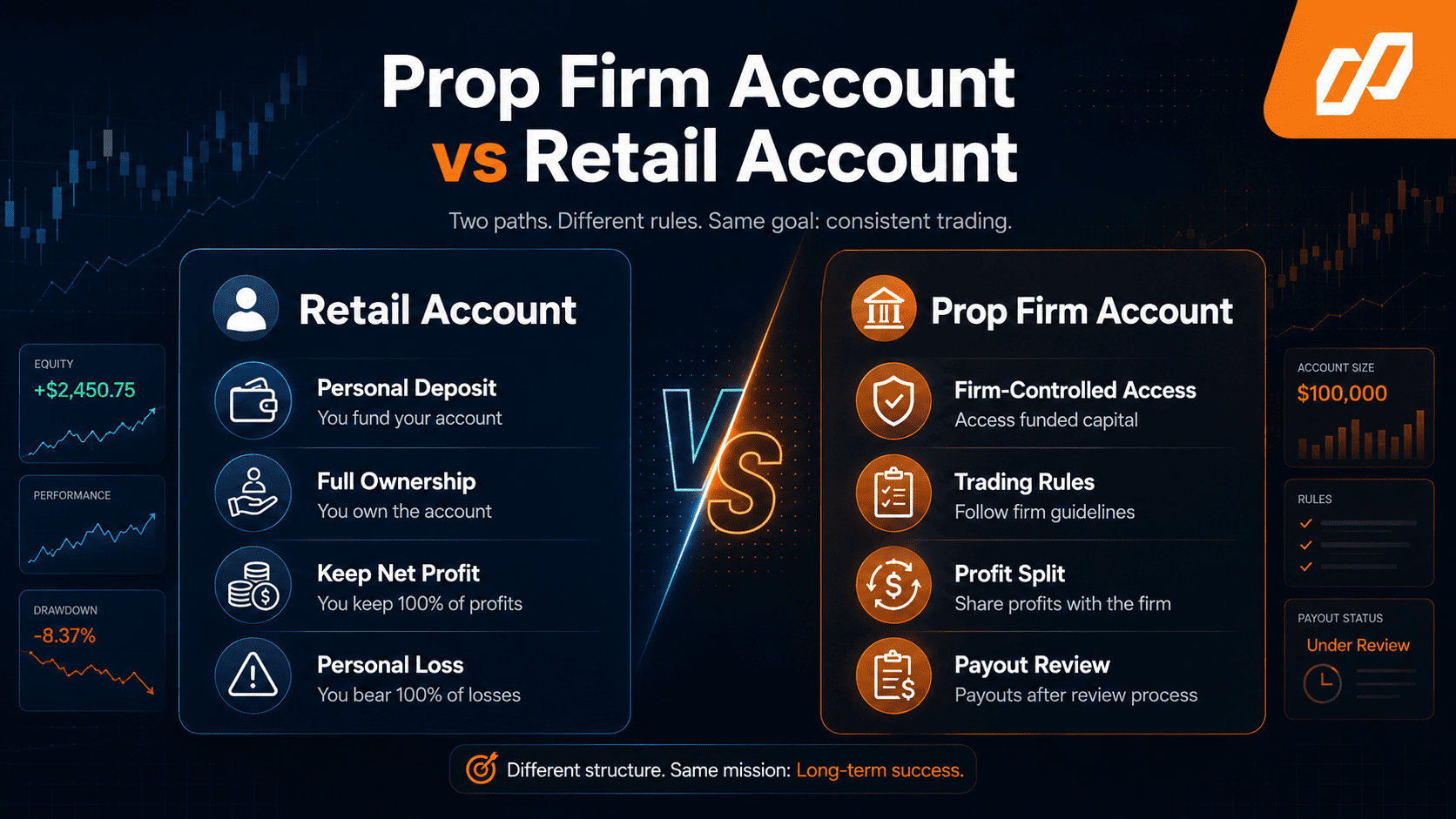

The simple difference is that a retail trader uses personal capital, while a prop firm trader uses conditional account access. But that explanation is incomplete. The real difference is control. A retail account is mainly capital-controlled. A prop firm account is rule-controlled.

| Account type | What the trader controls | What controls the trader | Main upside | Main risk |

|---|---|---|---|---|

| Personal retail account | Deposit size, broker choice, position sizing, strategy, withdrawals and account continuation | Broker margin, available capital, market losses, product terms and regulation | Direct ownership and full net profit after costs | Personal capital is exposed directly to losses |

| Prop firm account | Trade decisions inside the allowed account path | Daily loss, maximum loss, consistency, restricted trading, payout review and firm rules | Access to a larger account framework without depositing the full notional size | Account access and payout eligibility can be lost through rule breach |

That is why a profitable retail strategy can still fail inside a prop firm account. The trade may make sense financially, but the account can fail procedurally if it breaches the firm’s rule framework.

Retail Account Meaning: What Is a Personal Retail Trading Account?

A retail account is an individual trading account opened with a broker. The trader funds it with personal money and trades products the broker makes available, such as forex, indices, commodities, stocks, CFDs or other instruments depending on the broker and jurisdiction.

| Retail account layer | What it means | What the trader should remember |

|---|---|---|

| Capital ownership | The trader deposits and owns the account equity | Losses reduce personal capital directly |

| Profit ownership | The trader keeps net profit after trading costs, taxes and other obligations | There is no prop firm profit split |

| Broker controls | The broker controls margin, execution access, product availability, leverage and liquidation rules | Retail freedom still sits inside broker and legal terms |

| Withdrawal control | Withdrawals usually depend on available balance, broker processing and payment method | There is usually no prop-style payout eligibility review |

That makes a retail account more direct. The trader’s problem is simple to describe but hard to solve: protect personal capital and grow it without blowing up.

What Is a Prop Firm Account?

A prop firm account is a trading account or trading programme where the trader receives conditional access to capital, simulated capital or a funded-style environment controlled by the firm. The exact structure depends on the programme, but the trader is not operating like a normal retail account owner.

| Prop firm account layer | What it means | What the trader should remember |

|---|---|---|

| Conditional access | The trader receives access to a firm-controlled account path, not direct ownership of the displayed balance | Access can be removed if rules are broken |

| Rule framework | Daily loss, maximum loss, profit targets, consistency, holding, tools and restricted behaviour may apply | The account can fail even when the trader still sees a valid market idea |

| Profit split | Approved eligible profit is usually shared between trader and firm | The split matters only after profit becomes payout-ready |

| Account environment | The account may be simulated, monitored, copied, hedged or live-routed depending on the firm and stage | “Funded” should not be read as personal capital ownership |

For the firm-level definition, see what a prop trading firm is. For the funded-account definition, read what a funded trader account is.

Prop Firm Account vs Retail Account: Quick Comparison

The table below shows the practical difference between a prop firm account and a personal retail account.

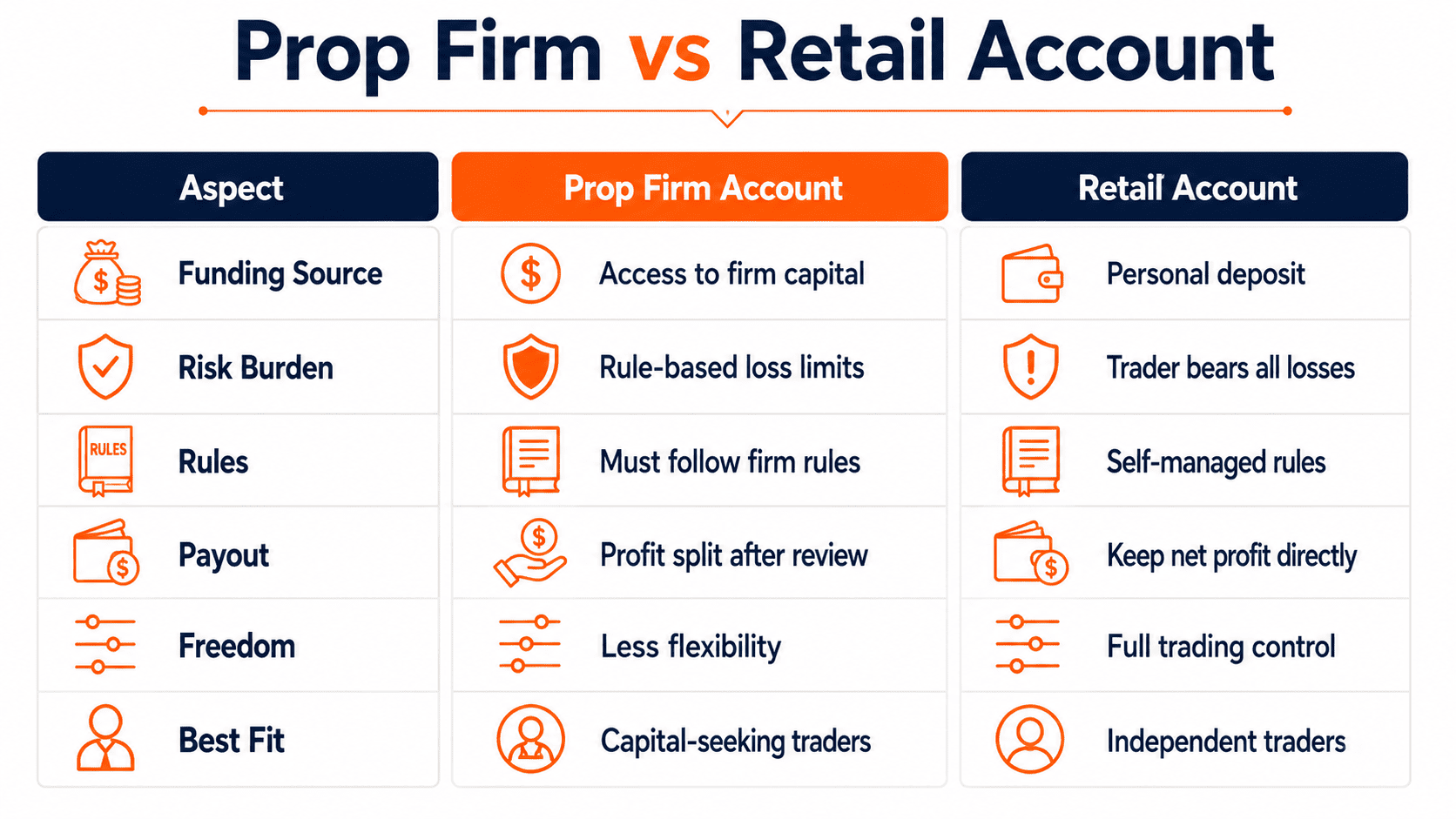

| Dimension | Prop firm account | Personal retail account | Why it matters | Detailed guide |

|---|---|---|---|---|

| Funding source | Firm-controlled capital access, funded-style account or simulated allocation depending on the programme | Trader’s own deposited capital | Prop trading gives access, while retail trading gives ownership | Do prop firms use real money? |

| Risk burden | Trader risks fees, account access, payout eligibility and rule status; firm controls the loss limits | Trader directly bears market losses from personal capital | Retail loss is mainly financial; prop loss can be procedural | Challenge costs |

| Rule system | Daily loss, max loss, trading restrictions, consistency, review and payout rules | Broker margin, liquidation, product and account terms | Prop accounts add a second rule layer above normal trading risk | Challenge rules |

| Profit structure | Profit split after compliance and payout approval | Full net profit after trading costs and other obligations | A high prop profit split only matters if the profit becomes eligible | Profit split explained |

| Payout and withdrawals | Subject to payout rules, minimums, buffers, review and account-specific terms | Withdrawals usually depend on broker processing and available account balance | Dashboard profit and withdrawable profit are not always the same in prop trading | First payout rules |

| Freedom and control | Limited by programme rules and allowed trading behaviour | More freedom, limited mainly by broker terms, margin and regulation | Some strategies fit retail but do not fit prop rules | Choosing checklist |

| Failure trigger | Rule breach, daily loss breach, max loss breach, payout violation or programme failure | Capital depletion, margin call, liquidation or voluntary stop | A prop account can fail before the trader has exhausted the notional account size | Why traders fail challenges |

| Best fit | Disciplined traders who can follow rules and want capital access without depositing the full account size | Traders who want full control, direct ownership and fewer programme restrictions | The better account depends on the trader’s behaviour, not only account size | Best prop firms for beginners |

Capital Source, Risk Burden and Rule Control

In a personal retail account, the trader owns the capital. In a prop firm account, the trader receives conditional access to a defined trading environment. That access can be removed if rules are broken.

| Control layer | Retail account | Prop firm account | Trader consequence |

|---|---|---|---|

| Capital source | Trader’s own deposited capital | Firm-controlled access, simulated or funded-style environment depending on programme | Retail trading gives ownership; prop trading gives conditional access |

| Primary objective | Grow and protect personal equity | Stay authorised inside the firm’s rules, then become payout-ready | Prop profit comes after rule survival |

| Bad day outcome | Account equity drops, and the trader chooses whether to continue if margin allows | The account may fail if daily loss, max loss or rule limits are breached | A prop account can end before the trader’s trade thesis has time to recover |

| Hard stop | Capital loss, margin call, liquidation or trader decision | Rule breach, loss-limit breach, payout violation or programme termination | Retail loss is mainly financial; prop loss can be procedural |

| Rules | Broker margin, leverage, product access, execution and withdrawal terms | Daily loss, maximum loss, consistency, trading days, restricted behaviour and payout review | A prop firm adds a second rule engine above normal trading risk |

| What the trader protects | Personal capital and broker account access | Account access, rule status, payout eligibility and trading process | Prop trading changes the form of risk; it does not remove risk |

If you are unclear on the loss mechanics, read daily drawdown vs max drawdown in prop trading. This is often where retail traders misjudge prop accounts.

The same trade can have different outcomes in the two account types. In a retail account, a floating loss may simply reduce equity. In a prop account, the same floating loss may breach a rule and end the account.

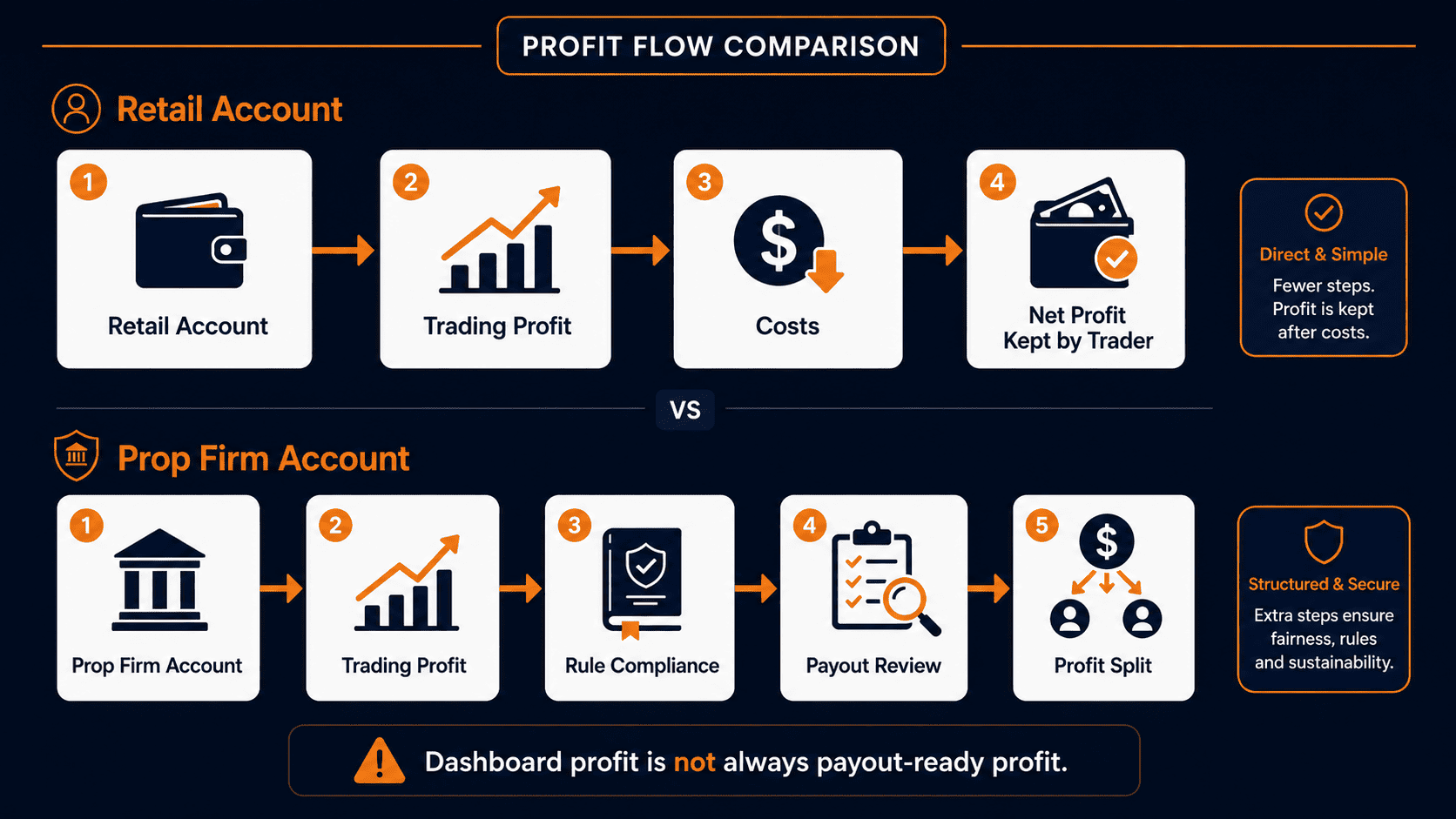

Profit, Payout and Freedom: Direct Ownership vs Payout-Ready Profit

In a retail account, profit belongs to the trader after trading costs and other obligations. In a prop firm account, profit is usually shared between the trader and the firm after the profit becomes eligible and approved.

| Control area | Retail account | Prop firm account | Trader mistake | Detailed guide |

|---|---|---|---|---|

| Profit ownership | Trader keeps net profit after costs, taxes and obligations | Trader receives a profit split after eligibility and approval | Comparing full retail profit with prop split without payout rules | Profit split explained |

| Withdrawal trigger | Available balance and broker withdrawal process | Payout request, KYC, account review and programme conditions | Thinking dashboard profit is already cash | First payout rules |

| Main blocker | Broker processing, payment method, compliance or insufficient available funds | Rule breach, payout minimum, consistency, buffer, open-position issue or review problem | Reading the split before reading eligibility | Why payouts get denied |

| Trading freedom | More freedom inside broker, margin and legal limits | Less freedom, more structure, stricter programme rules | Assuming a retail strategy transfers unchanged into prop rules | MT5 vs cTrader vs MT4 |

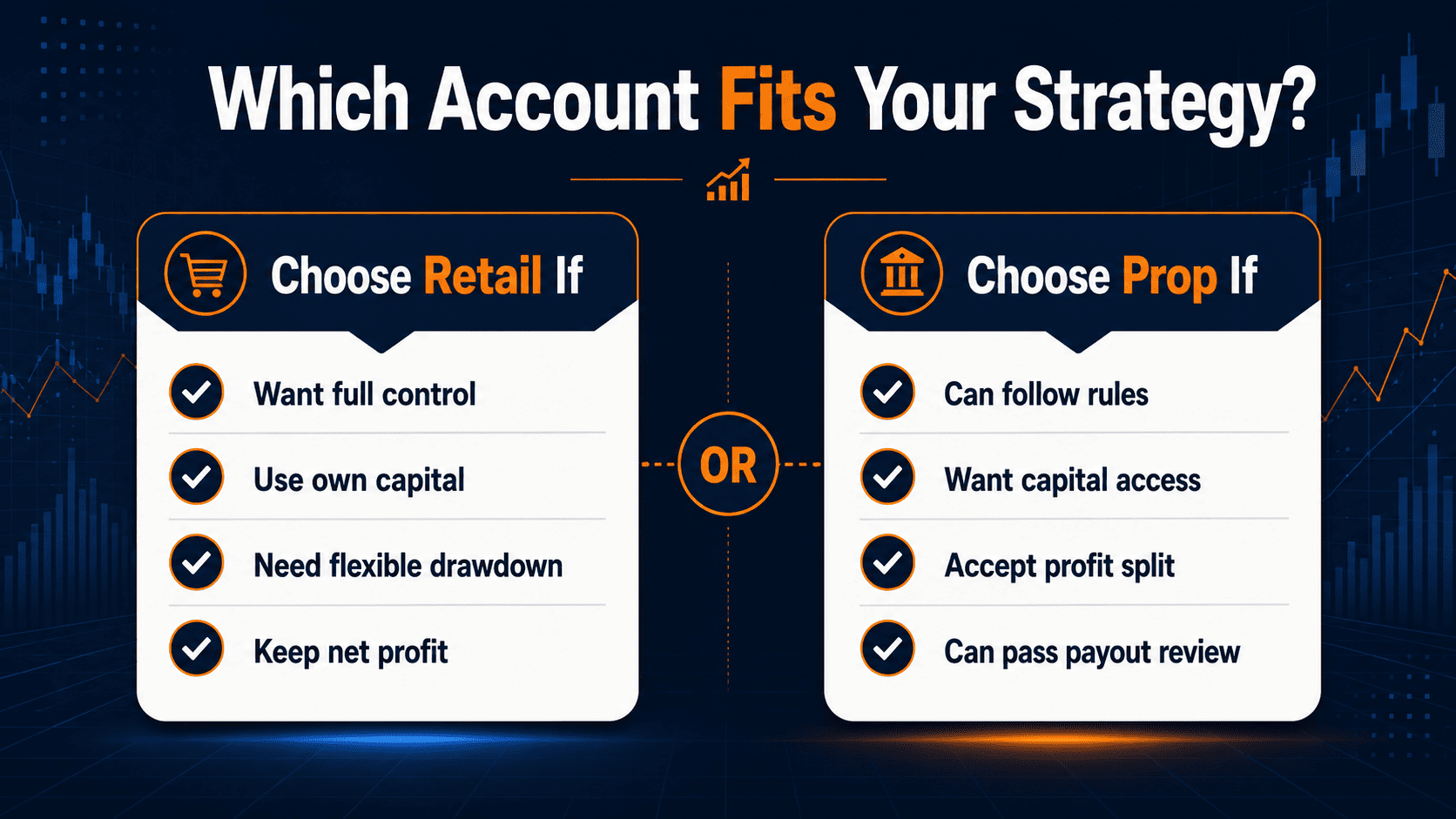

Who Should Choose a Retail Account?

A retail account is usually better for traders who want full control and are willing to accept full responsibility for losses.

- You want to trade your own money directly.

- You want to keep all net profit after costs.

- Your strategy needs wider stops, deeper temporary drawdown or longer holding periods.

- You do not want challenge targets, payout review or consistency rules.

- You can manage position size without external limits forcing discipline.

The danger is that freedom can expose poor discipline. A retail account gives control, but it does not protect the trader from over-sizing, revenge trading or holding losers too long.

Who Should Choose a Prop Firm Account?

A prop firm account is usually better for traders who have a tested process and can follow rules consistently.

- You want access to a larger account framework without depositing the full notional size.

- You can trade within daily loss and maximum loss limits.

- Your strategy produces controlled drawdown and repeatable execution.

- You are comfortable sharing profit in exchange for account access.

- You can follow payout rules without forcing extra trades.

The danger is that a prop account can make traders focus too much on passing and not enough on long-term execution quality. If you are comparing funded options, look past the headline split and read the AIFO trading rules before choosing.

Most traders do not fail because they cannot trade. They fail because the account model does not match the strategy.

If you are comparing funded options, check account models, drawdown logic, payout rules, platform limits and trading style fit before chasing a larger account label.

When a Retail Strategy Fails in a Prop Firm Account

A strategy can be profitable in a personal account and still be a poor fit for a prop firm account. This usually happens when the strategy needs room that the prop account does not allow.

| Strategy behaviour | Why it may work in retail | Why it may fail in prop | Detailed guide |

|---|---|---|---|

| Wide stops | The trader accepts deeper temporary drawdown | Daily loss or max loss rules may be too tight | Risk per trade |

| Holding through floating loss | The trader waits for recovery if margin allows | Floating drawdown may trigger a breach | Drawdown rules |

| Longer holding periods | The trader can wait for the trade thesis to develop | Overnight, weekend, swap or reset rules may add risk | Holding rules |

| Concentrated big winners | One large win can drive the account return | Consistency rules may block passing or payout | Consistency rule |

| High discretion | The trader can adapt freely | Programme rules may restrict news, sizing, instruments or behaviour | Challenge rules |

This does not mean prop accounts are worse. It means rule fit matters. A method that is profitable under one account structure can be unstable under another.

How to Decide Between a Prop Firm Account and a Retail Account

Do not choose based only on account size. Choose based on control, rules, payout path and actual trading behaviour.

| Question | Retail account is better if… | Prop firm account is better if… |

|---|---|---|

| Do you want full ownership? | You want direct control of capital and withdrawals | You accept conditional access in exchange for larger account exposure |

| Can your strategy handle tight rules? | Your method needs flexible drawdown tolerance | Your method already uses strict loss limits |

| How do you handle pressure? | You trade better without external targets | You trade better with defined limits and structure |

| How important is profit ownership? | You want to keep all net profit after costs | You accept a split because the account structure gives more opportunity |

| Can you follow payout conditions? | You want simpler withdrawal mechanics | You can wait for review and avoid forcing trades for payout |

| What is your biggest weakness? | You overreact to restrictions and targets | You over-risk when there are no external rules |

Common Mistakes When Comparing Prop and Retail Accounts

The comparison becomes misleading when traders focus on the account label instead of the account mechanics.

| Mistake | Why it is wrong | Better approach |

|---|---|---|

| Comparing prop account size with retail deposit size | A prop account size is conditional access, not personal capital ownership | Compare usable risk room, rules and payout path |

| Assuming a prop account has less risk | The trader may risk less personal capital, but can still lose fees, access and payout eligibility | Define both financial risk and procedural risk |

| Only looking at profit split | A high split does not matter if profit is not payout-ready | Check payout rules, review, buffers and minimums |

| Using the same lot-size logic in both accounts | Prop drawdown rules can be tighter than the trader’s retail tolerance | Size trades from the rule limit, not the headline account size |

| Ignoring strategy fit | Some profitable retail methods need too much recovery room for prop rules | Backtest the strategy against daily loss, max loss and payout rules |

Alpha Insight: Prop Accounts Are Behavioural Contracts

The shallow explanation says prop firms provide capital and impose stricter rules. The deeper explanation is more useful.

A retail account is a capital-constrained system. A prop account is a behaviour-constrained system.

The firm is not only limiting how much a trader can lose. It is defining what acceptable trading behaviour looks like: how quickly losses can accumulate, how much floating drawdown is tolerated, how consistently profit should appear, when payout can be requested and what execution patterns are considered acceptable.

That changes the question serious traders should ask. The right question is not “Which one gives me more leverage?” The right question is “Which account structure fits how my strategy behaves under pressure?”

Related Guides About Account Structure

- What is a funded trader account? — conditional access, simulated capital and payout eligibility.

- Do prop firms use real money? — real payout vs real execution vs real allocation.

- Prop firm payouts — how dashboard profit becomes payout-ready profit.

- Prop firm challenge rules — daily loss, max loss, consistency and restricted behaviour.

- What to check before choosing a prop firm — due diligence before buying an account.

Final Answer: Prop Firm Account vs Retail Account

A personal retail account gives direct ownership, direct profit, direct loss and more trading freedom. It is best for traders who want control and can manage their own capital responsibly.

A prop firm account gives conditional access to a larger trading environment, but the trader must follow programme rules and share profit after meeting payout conditions. It is best for traders with a tested process that can survive strict drawdown, consistency and payout rules.

The difference that matters is not the dashboard number. It is the structure underneath: who owns the capital, who controls the rules, who bears the risk, how profit becomes withdrawable and whether the trader’s strategy can survive the account model.

FAQ

A retail trading account is a personal brokerage account funded with the trader’s own money. The trader controls the deposit, places trades through the broker, keeps net profit after costs and absorbs losses from personal capital.

The main difference is ownership versus conditional access. A retail account uses the trader’s own capital. A prop firm account gives access to a firm-controlled trading programme where the trader must follow rules and usually shares approved eligible profit with the firm.

Not automatically. A prop firm account may reduce the need to deposit large personal capital, but it adds rule risk, evaluation fees, payout conditions and the possibility of losing account access. A retail account exposes personal capital directly but usually gives more control.

Not always. Many retail-facing prop firm accounts use simulated or monitored environments while still allowing approved rewards under the firm’s contract. AIFO’s current General Terms state that its services include simulated trading and fictitious demo funds unless expressly stated otherwise.

Usually no. Prop firm traders normally receive a profit split after meeting account rules and payout conditions. Retail traders generally keep their net trading profit after spreads, commissions, swaps, taxes and other applicable costs.

A profitable retail trader can fail a prop challenge because prop accounts judge both profit and rule compliance. A strategy that survives in retail may breach daily loss, maximum loss, consistency, news, overnight, tool-use or payout rules in a prop account.

A retail account usually gives more trading freedom because the trader controls the capital and is mainly limited by broker terms, margin, product access and regulation. A prop firm account limits freedom through programme rules and payout conditions.

A prop firm account is better suited to disciplined traders with a tested strategy that can operate inside strict drawdown, consistency, execution and payout rules. It is not ideal for traders who need wide recovery room or dislike external restrictions.

A retail account is better suited to traders who want direct ownership, full control and full net profit after costs. It also suits strategies that need more flexible holding periods, wider stops or deeper temporary drawdown tolerance.