The cheapest prop firm path is not the smallest fee on the checkout page. It is the lowest total path to a clean, eligible payout. That means you must count the challenge fee, reset risk, subscription cost, activation fee, data fee, payout buffer, minimum withdrawal, review rules and payment costs. A cheap account is useful only if it does not push you into oversized trades or repeated resets. The safer low-cost route is simple: test first, pay small, protect the account, then withdraw only when the profit is clean.

What is the cheapest prop firm path?

The cheapest path is the one that reaches the first clean payout with the fewest paid mistakes. It is not always the lowest advertised challenge fee.

A low price can still be expensive if it creates a reset loop. A higher fee can be cheaper if the rules are clear, the payout route is clean and the trader does not need to buy the same account again.

This is the first mistake traders make when comparing firms. They compare the payment today. They ignore the cost of failing, resetting, activating, waiting, fixing consistency and submitting a payout that may not yet be eligible.

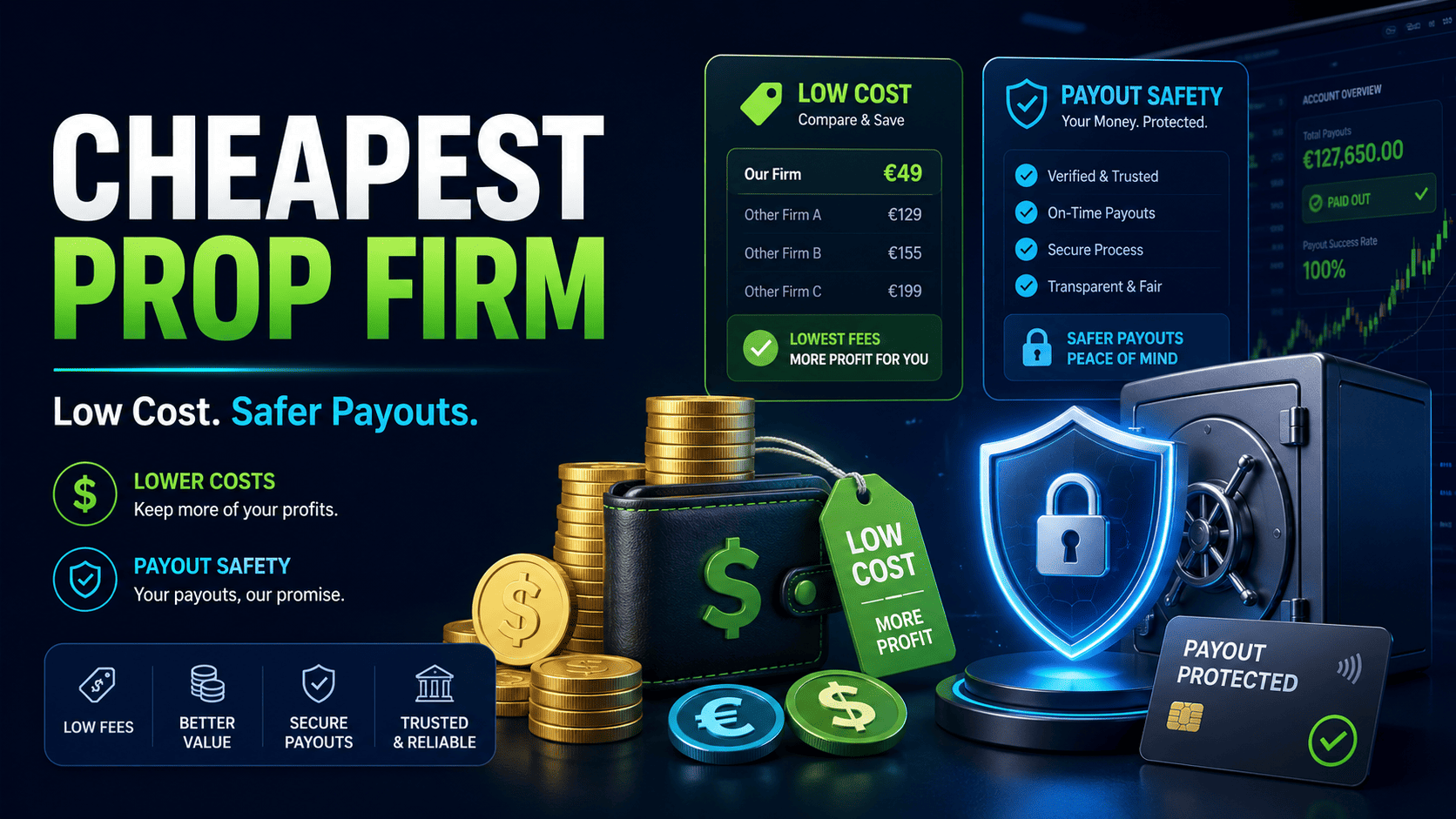

Read prop firm challenge fees compared in 2026 before treating a fee as the full price. The fee is only the first line of the bill.

Why the cheapest checkout price can be the wrong choice

A cheap checkout price can hide the real cost of the account path. The trader pays less at the start, then pays more through resets, activation fees, tighter rules or slow payout access.

This is where low-budget traders get hurt. They buy the smallest entry point, then trade too aggressively because they want the fee back quickly.

That behaviour turns a cheap challenge into a high-cost loop. One failed attempt becomes two. Two become five. The trader keeps searching for a cheaper firm while repeating the same failure path.

The right question is not “What is the lowest fee?” The right question is “What is the lowest cost to reach a payout without breaking the account?”

| Cost layer | What traders usually see | What they often miss | Safety check |

|---|---|---|---|

| Entry fee | The advertised challenge price | The account may have tighter rules or a longer path | Check the rule box before the price |

| Reset cost | A small second chance | Repeated resets can exceed a higher-quality account | Stop paying until the failure reason is fixed |

| Subscription cost | A low monthly payment | Time pressure and recurring fees change behaviour | Count months to pass, not only month one |

| Activation fee | Not always shown beside the challenge fee | Passing may trigger another payment before funding | Add after-pass cost to the total path |

| Data or platform fees | Often treated as small extras | They compound across failed attempts | Include them before comparing firms |

| Payout friction | A high profit split or fast payout claim | Minimum withdrawal, buffer, review and payment fees | Check payout eligibility before buying |

The cheapest safe route starts with testing, not paying

The lowest-risk starting point is a trial or simulation that exposes your behaviour before you attach money to the attempt. The goal is not to make money in the trial. The goal is to find out how you behave under rules.

This is why an AIFO free trial account has real value for a low-budget trader. It lets you test the process before the paid attempt starts.

A trial should not be treated like a toy account. Trade it with the same daily stop, risk per trade, session rules and trade count you would use in the paid challenge.

If you overtrade in the trial, you will probably overtrade in the paid account. If you break the daily stop in simulation, a cheaper challenge will not fix that. It will only make the same mistake easier to repeat.

How to balance low cost with payout safety

Balance low cost with payout safety by checking both sides of the path: what you pay before funding and what must happen before profit can leave the account. A cheap entry means little if the payout rules are hard to satisfy.

Payout safety is not a slogan. It is a rule-state question.

Ask whether the profit is eligible. Ask whether the account has a buffer. Ask whether the best day is too large. Ask whether payment fees apply. Ask whether the account can still trade safely after withdrawal.

The AIFO payout process is a useful model for this thinking. A payout is not just a button. It is a sequence from profit to eligibility, review and payment.

| Payout safety field | What it controls | Low-budget risk | Cleaner action |

|---|---|---|---|

| Minimum withdrawal | How much must be available before a request | Small profits may not be withdrawable yet | Plan trade size around realistic payout thresholds |

| Payout buffer | Profit that must remain in the account | The trader expects to remove more than is available | Calculate withdrawable profit before sizing up |

| Consistency rule | Profit distribution across days | One big day can force more trading | Cap daily profit before the ratio becomes a problem |

| Review process | Whether the account activity is accepted | Fast profit may still be questioned | Trade in a way that looks repeatable and rule-clean |

| Payment method | How the payout reaches the trader | Fees or limits reduce the final amount | Check payment rails before the first request |

| Post-withdrawal drawdown | How much room remains after payout | The account becomes fragile after removing profit | Leave enough room to keep trading safely |

Why high profit split is not the same as payout safety

A high profit split is attractive, but it does not prove that the payout path is clean. The split applies only after the rules decide what profit is eligible.

This is why prop firm payouts should be read as a system, not a percentage.

A 90%, 95% or even 100% split can still be weak if the account has tight payout caps, unclear review language, a strict consistency rule or a difficult minimum withdrawal threshold.

The trader sees the split. The firm reviews the path of the profit. Those are different things.

A low-budget trader should prefer a smaller, clearer payout path over a flashy split with hidden friction. You do not get paid from the headline. You get paid from eligible profit.

How payout buffers change the real cost

A payout buffer changes how much of the account profit can actually be withdrawn. It can make the first payout smaller than the trader expected, even when the account is profitable.

This is not a bad rule when it is clear. It protects the account from becoming too fragile after a withdrawal.

The AIFO payout buffer requires traders to retain a 2% profit buffer based on the initial account balance when requesting withdrawals. That means the trader should calculate payout-available profit before thinking about the split.

This is where cheap-path planning becomes practical. A trader who ignores the buffer may overestimate the first payout, then trade again to “make the withdrawal worth it”. That extra trade is often where the account gets damaged.

The safer move is to know the buffer first, then size the account path around it.

The low-budget trader’s biggest hidden cost is behaviour

The biggest hidden cost is not always a fee. It is the behaviour that cheap accounts encourage.

A trader who thinks the account is cheap may treat the rules cheaply too.

That usually shows up in three ways. The trader takes more trades because the fee feels small. The trader resets too quickly because the next attempt feels affordable. The trader sizes too large because they want to recover the fee fast.

This is where why traders fail prop firm evaluations becomes part of the pricing decision. A failed account is not only a trading loss. It is a cost item.

Cheap accounts can be useful for disciplined traders. They are dangerous for traders who use price as permission to experiment.

Build a cost-to-first-clean-payout plan

The best low-cost plan measures the cost to the first clean payout. This is a better metric than challenge fee because it includes both money and rule friction.

Build the plan before buying the account. Do not build it after the first failed attempt.

Use this sequence:

- Start with a trial or simulation if your behaviour is untested.

- Choose a small account only if the rules fit your strategy.

- Add every visible fee before comparing options.

- Check the payout buffer, minimum withdrawal and review rules.

- Set a personal daily stop below the firm limit.

- Stop after a failed attempt and diagnose the failure before paying again.

The risk management strategy should sit inside the cost plan. Without it, the cheapest path becomes a repeated purchase path.

The decision matrix for choosing a cheap but safer path

A low-budget trader should compare account paths by fit, not by price alone. The right path is the one that gives the strategy enough room and gives the payout process enough clarity.

This matrix is a cleaner way to compare cheap routes.

| Path type | Why it looks cheap | Main payout safety risk | Best use case |

|---|---|---|---|

| Free trial first | No paid challenge pressure | No profit sharing or funded account outcome | Testing behaviour, rule awareness and strategy fit |

| Small staged challenge | Lower first payment | Longer route and more chances to break rules | Disciplined traders who can repeat process across phases |

| Subscription model | Low first month fee | Recurring cost, after-pass fees and payout caps | Fast, structured traders who understand the clock |

| Instant-style account | No long evaluation path | Higher price or stricter payout conditions | Experienced traders with tested risk control |

| Higher-trust, higher-fee route | Not the cheapest upfront | Higher initial cost | Traders who value rule clarity and payout process over discounts |

Use choosing a funded trading firm as the wider filter. A cheap path is still a bad path if it forces your strategy into behaviour that does not fit the rules.

Alpha Insight: cheap becomes expensive when the mistake repeats

The cheapest prop firm path is not the smallest payment. It is the shortest path to a clean, eligible payout without buying the same mistake twice.

That is the difference most traders miss.

A cheap account can be a smart entry point. It can also become a loop. The difference is diagnosis.

If you fail because of a daily loss breach, do not buy another account until the daily stop is fixed. If you fail because the rules did not fit your holding time, do not buy a cheaper version of the same mismatch. If you reach profit but cannot request payout, do not call it bad luck before checking eligibility.

The article why some prop firms are bad deals in 2026 makes the same point from the other side. A bad deal is not always expensive at checkout. Sometimes it is cheap at checkout and expensive in behaviour.

Final answer: the safest cheap path

The safest cheap path is trial first, small paid account second, clean payout rules third. Do not reverse that order.

Start by testing behaviour. Then choose the lowest-cost account that fits your strategy. Then check payout eligibility before chasing a bigger account or a higher split.

Read the AIFO payout rules before thinking of profit as withdrawable. The trader who understands the payout path before paying usually spends less than the trader who learns it after reaching the target.

Cheap is good only when it keeps you rational. The moment it makes you careless, it is no longer cheap.

FAQ: Cheapest prop firm path and payout safety

The cheapest path is the lowest total route to a clean payout, not the smallest checkout fee. It should include the challenge fee, resets, subscription cost, activation fee, payout buffer, minimum withdrawal and review risk.

No. A cheap challenge can become expensive if it leads to repeated resets, unclear payout rules, strict consistency limits or behaviour that damages the account before the first withdrawal.

Check the minimum withdrawal, payout frequency, profit split, payout buffer, consistency rule, review process, payment fees and any account status rule that can stop profit from becoming eligible.

A payout buffer keeps some profit in the account after withdrawal so the account still has risk room. It reduces the immediately withdrawable amount, so traders should calculate it before expecting a first payout.

Yes. A free trial helps test rule awareness, daily stop discipline, strategy fit and trade behaviour before paying for a challenge. It is not a payout route, but it can prevent paid mistakes.

The biggest hidden cost is repeated failure. A low fee becomes expensive when the trader keeps resetting the same mistake, trades too large to recover the fee, or reaches profit that is not payout-eligible.