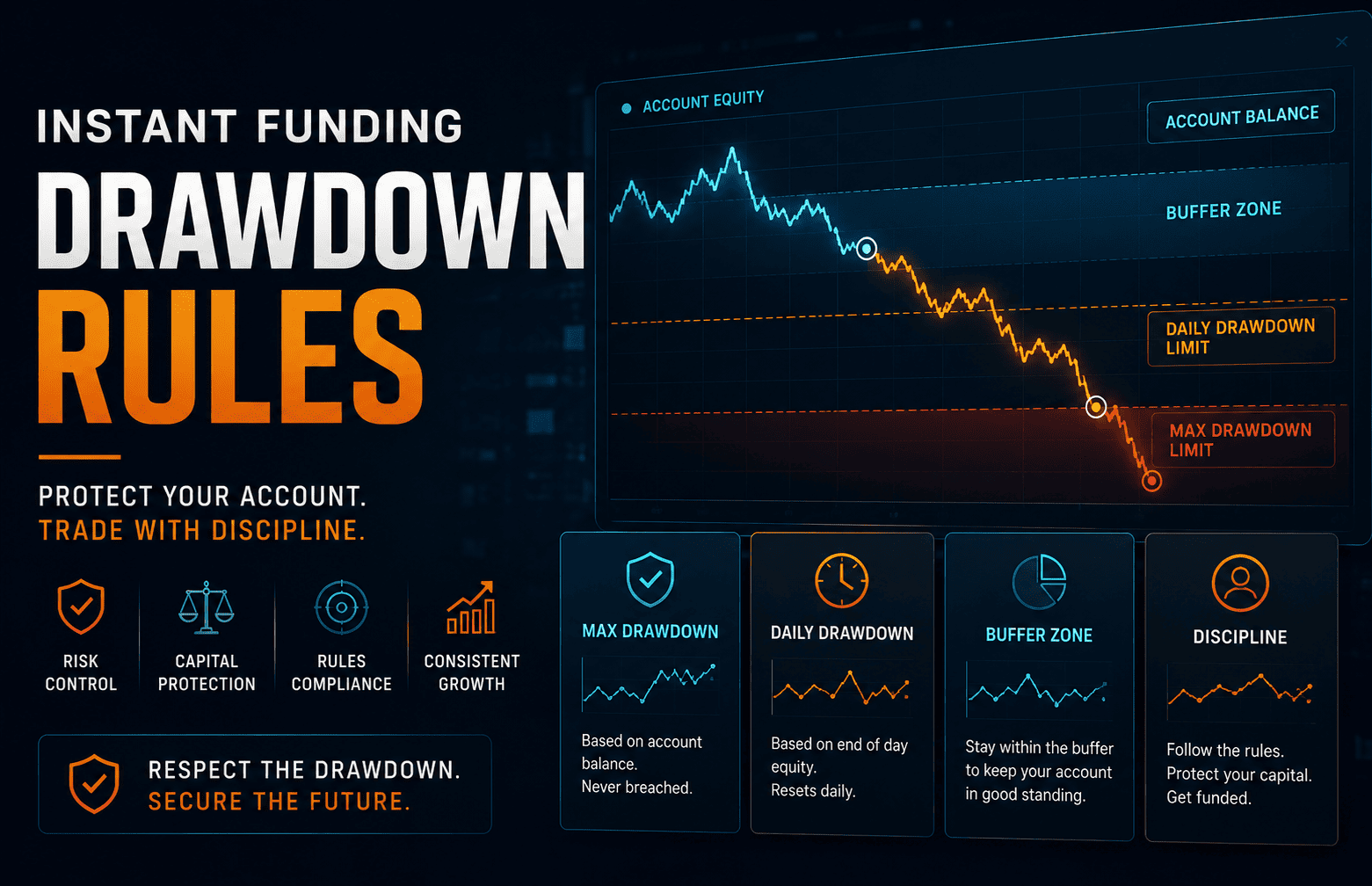

Instant funding drawdown rules define the usable room between current equity and the nearest account boundary. Faster access does not remove the risk engine. Daily loss, maximum loss, single-trade floating loss, consistency, payout buffer and payout review can all control whether an instant account remains tradable. Start with the AIFO Instant Funding program for the account path, then use this guide to understand how drawdown affects first payout and account survival.

Instant funding looks clean because there is no long challenge phase in front of the account. That does not make the account loose. It means the account-state test starts earlier.

This article is the drawdown-risk child guide for Instant Funding. Use the broader daily, maximum and trailing drawdown guide for general drawdown mechanics. Use this page for the Instant-specific question: how daily loss, maximum loss, single-trade floating loss and payout buffer can reduce real trading room before or after the first withdrawal.

Instant Funding Drawdown Rules Are an Account-State Map

Instant funding removes the waiting room. It does not remove the walls. The account may be active faster, but the drawdown rules usually begin from the first trade.

| Instant-account boundary | What it controls | Common trader mistake | What to check before trading |

|---|---|---|---|

| Daily loss | The account’s one-day survival room | Treating the daily percentage as fully usable risk | Reference value, reset time, open P&L, commission and swap treatment |

| Maximum loss | The lifecycle survival floor for the account | Sizing from the account balance instead of the nearest loss floor | Static, trailing, equity high-water-mark or account-specific logic |

| Single-trade or floating-loss cap | The maximum damage one trade or open exposure can create | Thinking the daily loss rule is the only intraday limit | Whether one trade has a separate hard cap before daily loss is reached |

| Consistency | How concentrated account profit can be | Letting one instant-account win dominate the payout period | Single-day, best-day, top-two-day and dashboard formulas |

| Payout buffer | The amount that must remain after withdrawal | Treating dashboard profit as fully withdrawable | Buffer formula, full-withdrawal consequence and post-payout risk room |

The account balance shown on the dashboard is not the trading room. The trading room is the distance between current equity and the nearest active boundary.

Identify the Drawdown Model Before You Size the First Trade

Do not trade an instant account from the label “static”, “trailing” or “smart”. Write down the actual formula. The same phrase can behave differently depending on whether the firm uses balance, equity, end-of-day values, highest historical equity or a payout-triggered floor.

| Drawdown model | How it usually behaves | Instant-account danger | What the trader should verify |

|---|---|---|---|

| Static or fixed drawdown | The breach floor is usually tied to an initial or fixed reference value | The rule is easier to model, but early losses still reduce the account’s target path and payout room | Initial reference, equity treatment, fees, commissions and whether payout changes the floor |

| Balance-based trailing drawdown | The floor can move after closed balance reaches a new high | Closed profit can tighten future loss room before the trader expects it | Whether the floor trails intraday, at end of day or after closed results only |

| Equity high-water-mark drawdown | The floor can move when equity reaches a new high, even while trades remain open | Unrealised profit can reduce future breathing room before profit is secured | Whether open P&L moves the floor and whether the floor ever locks at a cap |

| Smart or step drawdown | The floor may change after a defined profit threshold, payout event or account milestone | The account can feel safer after profit while the rule has actually tightened | Trigger point, post-trigger floor, payout consequence and account-status change |

| Payout-adjusted floor | The account may need to retain profit or buffer after withdrawal | Withdrawing too much can leave the account too close to breach | Buffer, full-withdrawal rule, post-payout equity and next-day daily loss floor |

The wider daily, maximum and trailing drawdown guide explains the general models. On an Instant account, the practical question is narrower: which floor is closest now, and what happens to that floor after profit or payout?

Daily Loss and Equity Rules Can Breach the Account Before the Trade Closes

Daily loss is the fastest account boundary because it works inside one server-defined trading day. It can breach the account before the trader has time to recover.

The dangerous part is calculation. Some firms use balance. Some use equity. Some use the higher of the two. Some recalculate at server rollover. If equity counts, floating loss matters.

| Field to check | Question | Instant-account consequence |

|---|---|---|

| Daily reference | Does the day use starting balance, previous close, closing equity or the higher value? | The new day can begin with less room than the trader expects |

| Open P&L | Can floating loss breach the account before the trade closes? | A trade can later recover but still have touched the rule line earlier |

| Costs | Are commission, swap and spread included in the daily loss calculation? | A stop that looks safe on the chart can be too large after costs |

| Server time | When does the daily rule reset according to the account clock? | A trade held through reset can be judged under a new floor |

| Personal stop | Where does the trader stop before the firm’s hard line? | The personal stop prevents the account from being managed at the cliff edge |

Current AIFO Daily and Maximum Loss References

Last checked on : AIFO’s public rules state that Instant Funding uses a 2% Daily Drawdown and a 2% single-trade floating loss control. AIFO’s daily loss wording states that the Daily Loss Limit is based on the previous day’s closing balance or equity, whichever is higher, and that commissions, swaps, open P&L and closed P&L can affect the floor.

Daily loss floor = higher of previous-day closing balance or closing equity × (1 − daily loss percentage)

| AIFO Instant example | Calculation | Meaning |

|---|---|---|

| $50,000 Instant account, 2% Daily Drawdown | $50,000 × 98% = $49,000 | Equity must remain above the current daily floor |

| Previous-day closing equity rises to $52,000 | $52,000 × 98% = $50,960 | The new daily floor can be higher after account growth |

| One trade floating loss approaches 2% of initial balance | $50,000 × 2% = $1,000 | The trade can be too large even before the daily floor is reached |

AIFO’s maximum loss wording also matters because the floor can move when the account reaches a new equity high and does not move back down when equity falls. Read the AIFO daily loss limit, AIFO maximum loss limit and AIFO server time before sizing an Instant trade.

Payout Risk: Why Withdrawal Can Reduce Survival Room

Payout is not just money leaving the firm. It is also profit leaving the account. If the account must retain a buffer, or if the loss floor remains close after withdrawal, the account can become fragile after a successful payout.

This is one of the most ignored Instant Funding risks. Traders celebrate the payout and forget that the next trade still has to survive the remaining buffer.

Last checked on : AIFO’s public payout buffer FAQ states that traders must retain a profit buffer equal to 2% of the initial account balance when requesting withdrawals. It also states that withdrawing the full profit, including the buffer, automatically closes the account.

Payout-available profit = account profit − required payout buffer

| Example field | Amount | Meaning |

|---|---|---|

| Initial account balance | $50,000 | The account reference used for this example |

| Required 2% payout buffer | $1,000 | $50,000 × 2% |

| Account profit | $3,500 | Dashboard profit before buffer and split treatment |

| Payout-available profit before split | $2,500 | $3,500 − $1,000 |

This does not mean payouts are bad. It means withdrawal size is part of drawdown management. A clean payout is not always the largest payout. It is the payout that leaves the next trading day tradable.

Payout Review Can Expose Hidden Drawdown Problems

A payout request often brings the account under closer review. Open trades, daily loss history, max loss history, consistency, restricted behaviour and account state can all matter.

A profitable account is not automatically payout-ready. It must be rule-ready.

Before requesting a withdrawal, read the AIFO payout process, AIFO payout buffer FAQ and instant funding payout rules. Check buffer, open-position state, rule history, KYC and payout conditions before the account is under review.

Rule Stack Table: How Instant Funding Drawdown Changes Execution

The safest way to read instant funding drawdown rules is as a stack. Each rule limits a different part of the account path. The account fails when the trading path touches the nearest active line.

| Rule layer | What traders often think | What it really limits | Execution consequence | Common failure path | Detailed guide |

|---|---|---|---|---|---|

| Daily loss | “I can lose this percentage today.” | Intraday equity damage, floating loss and emotional recovery trading | Requires a personal stop before the firm limit | Floating loss touches the daily line before the trade recovers | Daily loss reset time |

| Maximum loss | “The account can lose this much overall.” | The account-level survival floor across the active phase | Risk per trade must be built from the nearest floor, not the headline balance | Trader loses early, then increases size to recover the account | Drawdown rules |

| Single-trade floating-loss cap | “It only matters if I hit daily loss.” | How much one open trade can damage the account before other rules are reached | One large idea can be invalid even when daily loss room remains | Trader treats the whole daily limit as trade-level risk | Risk per trade |

| Consistency | “Consistency is a payout detail.” | Whether profit is distributed in a repeatable way | A strong day needs a best-day and top-two-day check before more risk is added | One instant-account winner creates payout-readiness pressure | Consistency rule |

| Payout buffer | “Payout is separate from drawdown.” | The survival room left after profit leaves the account | Withdrawal size must leave enough room for the next losing day | Trader withdraws too much, then breaches on a normal pullback | Instant funding payout rules |

| Payout review | “Profit on the dashboard is mine.” | Whether the account, strategy, KYC and payout destination pass review | Trading should slow down before the account enters review | Profit exists, but the account is not payout-ready | Why payouts get denied |

How to Trade Around Instant Funding Drawdown

Trade from the breach line backwards. Do not start with the account size. Start with the nearest active rule boundary and ask how much loss the next trade can create.

| Trading step | Question before action | Block the trade or payout if |

|---|---|---|

| Before the first trade | Which boundary is closest: daily loss, maximum loss, single-trade cap or personal stop? | The trader cannot calculate the current failure buffer |

| After a loss | Does the next normal loss still fit inside the personal daily stop? | The next trade requires perfect execution to stay safe |

| After a strong profit day | Did the best-day or top-two-day concentration become too high? | More trading would make the account less payout-ready |

| Before holding through reset | Will the new server day recalculate the daily floor from a higher reference? | The account may become tighter after reset |

| Before payout request | How much buffer remains after the requested withdrawal? | The account would be fragile or close under full-withdrawal rules |

Alpha Insight: Instant Funding Is a Buffer Contract

Instant funding drawdown rules do not mainly decide how much you can lose. They decide how much of your profit is actually usable.

Profit can raise the daily reference. Profit can increase consistency pressure. Profit can become unavailable if payout conditions are not met. Profit can leave the account through withdrawal and take the survival cushion with it.

The instant account is not only asking, “Can you make money?” It is asking, “Can your account path keep enough buffer while you make money?”

That is a different test.

Using AIFO Rules as the Final Check

Last checked on : AIFO Instant currently uses no traditional evaluation phase, 2% Daily Drawdown, 2% single-trade floating loss, 5% Maximum Loss for Standard, 4% Maximum Loss for Elite / No Commission, 15% single-day concentration, 25% top-two-day concentration and payout on demand under the public rules.

| AIFO Instant item | Current public rule or process | Trader action | Official reference |

|---|---|---|---|

| Account path | No traditional evaluation | Do not treat faster access as lower risk | AIFO Instant Funding |

| Daily Drawdown | 2% | Set a personal daily stop before the firm’s daily floor is threatened | AIFO trading rules |

| Single-trade floating loss | 2% of the initial account balance for Instant accounts | Do not use the hard cap as normal working risk | AIFO trading rules |

| Maximum Loss | 5% for Standard; 4% for Elite and No Commission | Check the exact account type before calculating the floor | AIFO trading rules |

| Consistency | 15% single-day concentration and below 25% top-two-day concentration under current public rules | Track best-day and top-two-day profit before adding more risk | AIFO trading rules |

| Payout path | Payout on demand after applicable withdrawal, consistency, review and account-specific rules are met | Do not treat dashboard profit as approved cash | AIFO payout process |

The right rule read should produce a trade plan, not just understanding. It should tell you the daily stop, maximum position risk, payout buffer and point where trading stops for the day.

Related Guides for Instant Funding Drawdown

- Instant funding payout rules — first withdrawal, buffer, KYC, review and payout-on-demand conditions.

- Daily, maximum and trailing drawdown — broader drawdown mechanics and examples.

- Daily loss reset time — server time, reset reference and cross-day breach risk.

- Risk per trade in a prop firm challenge — position sizing from failure buffer instead of account balance.

- Why prop firm payouts get denied — evidence and review checks when payout is delayed or rejected.

FAQ

Instant funding drawdown rules are the daily, maximum, floating-loss and account-state limits that control how far an instant account can move before it breaches, freezes, becomes restricted or fails payout readiness. They may include daily loss, maximum loss, single-trade caps, consistency rules and payout buffer requirements.

It can feel stricter because the account starts under account rules immediately, without a diagnostic evaluation phase first. Faster access does not mean wider risk room. Daily loss, maximum loss, consistency, payout review and buffer rules can apply from the first trade.

AIFO’s current public rules list Instant Funding with 2% Daily Drawdown, a 2% single-trade floating-loss rule, 5% Maximum Loss for Standard accounts and 4% Maximum Loss for Elite / No Commission accounts. Traders should verify the live AIFO trading rules and dashboard before trading.

Yes, when the firm calculates daily loss, maximum loss or single-trade limits using equity or open P&L. Equity includes open profit and loss, so an open trade can breach the account before it is closed. AIFO Instant also has a current public 2% single-trade floating-loss rule.

Payout creates drawdown risk because profit may leave the account while the account still needs enough buffer to keep trading. Under AIFO’s current public buffer rule, traders must retain a profit buffer equal to 2% of the initial account balance when requesting withdrawals, and a full withdrawal including the buffer closes the account.

Size trades from the nearest active breach line backwards. Calculate the loss if the stop is hit, including spread, commission, swap, slippage and floating movement. If that loss puts the account close to daily loss, maximum loss, single-trade floating loss or post-payout buffer pressure, the trade is too large for the account.

No. Payout on demand means the trader can request payout when the applicable conditions are met. It does not mean every profitable trade is immediately withdrawable. The account may still need consistency, review, KYC, open-position, payout-destination and buffer checks.