To pass a futures prop firm challenge, plan from the loss line backwards before chasing the profit target. Futures challenges are contract-risk tests: stop distance, tick value, number of contracts, session volatility, drawdown rules and payout-review conditions decide whether the account path survives. Use the How to Pass a Prop Firm Challenge Hub for the full passing roadmap, then use this page for futures-specific buffer, tick-risk and contract-sizing planning.

Do not copy a forex-style percentage plan directly into futures. A futures trade must be translated into contracts, ticks and exchange-session behaviour before it becomes a usable risk number. One extra mini contract can turn a controlled idea into a rule breach.

Important scope note: this is an educational futures challenge guide. It should not be used as proof that every prop firm account offers exchange-traded futures. If you are trading an AIFO account, verify the actual products, platform specifications and live account rules before applying any futures contract example.

How to Pass a Futures Prop Firm Challenge Without Forcing the Target

The right way to pass a futures prop firm challenge is to protect the account path first. The profit target matters, but it comes after the account can survive normal futures movement.

Most failed attempts start with the wrong question: “How much do I need to make per day?” That sounds organised, but it pushes the trader toward target pressure. Futures traders need a different first question: “What is the smallest contract risk that lets my setup work while keeping the account eligible?”

| Planning question | Wrong target-first answer | Better futures-risk answer | Guide to use |

|---|---|---|---|

| How much should I trade? | Enough contracts to reach the target quickly | The number of contracts that fits stop distance, tick value, daily loss room and max-loss room | Risk per trade |

| How fast should I pass? | As fast as possible | As fast as the account can progress without forced trades, consistency pressure or drawdown damage | Challenge roadmap |

| When should I scale? | After one strong trade or one strong day | Only after realised buffer exists and the next full stop still fits the plan | Risk management strategy |

| When should I stop? | After the market stops moving | At the written daily loss stop, daily profit stop, behaviour stop or pass-ready stop | Day 1 checklist |

The challenge is not passed by being aggressive every session. It is passed by staying eligible long enough for good trades to matter.

Futures Challenges Are Contract-Risk Tests, Not Percentage-Return Tests

Futures risk is built from contracts, ticks and stop distance. A percentage risk rule becomes useful only after it has been translated into actual contract exposure.

Trade risk = stop distance in ticks × tick value × number of contracts

Maximum contracts = allowed money risk ÷ (stop distance in ticks × tick value)

| Example field | Example value | Meaning |

|---|---|---|

| Allowed money risk | $240 | The maximum this trade is allowed to lose after the failure-buffer calculation |

| Stop distance | 24 ticks | The distance between entry and invalidation |

| Tick value | $2 per tick | Example tick value for the contract being traded |

| Risk per contract | $48 | 24 ticks × $2 |

| Maximum contracts | 5 contracts | $240 ÷ $48, before any extra slippage or cost cushion |

Example note: This table uses a simplified tick-value example. Real tick value, tick size, commission, exchange fees, margin treatment and platform specifications vary by instrument and firm. Verify the exact contract specification before using the formula.

Micro Contracts Are Not a Beginner Weakness

Micro contracts are often the cleanest way to pass a futures prop firm challenge because they give finer control over stop placement, scaling and daily loss exposure. Minis can be efficient, but they also make small errors expensive.

The trader who starts with micros can test the session, read volatility and build realised buffer before increasing size. The trader who starts with minis is often trying to compress the challenge into fewer decisions. That creates pressure. Pressure creates bad entries.

There is no prize for using the largest contract size allowed. The account only cares whether the rule path survives.

Correlated Futures Exposure Counts as One Risk Event

ES, NQ, YM and RTY do not move identically, but they often react to the same equity-index shock. A trader holding several index positions may think they are spreading risk. In reality, they may be stacking one theme.

This matters during a challenge. A loss on NQ, ES and YM in the same move is not three independent mistakes. It is one oversized exposure split across instruments.

| Exposure type | Wrong treatment | Cleaner risk treatment |

|---|---|---|

| Several equity-index futures positions | Count each symbol as a separate low-risk trade | Treat them as one index-risk cluster and cap the combined stop loss |

| Futures plus correlated CFD or index exposure | Assume different platforms mean separate risk | Combine exposures by market driver before sizing |

| Energy, metals or rates positions during macro news | Assume different sectors remove event risk | Check whether the same event can move all positions together |

Build the risk plan around clusters. Do not count separate symbols as safety unless the account plan treats them as separate and capped.

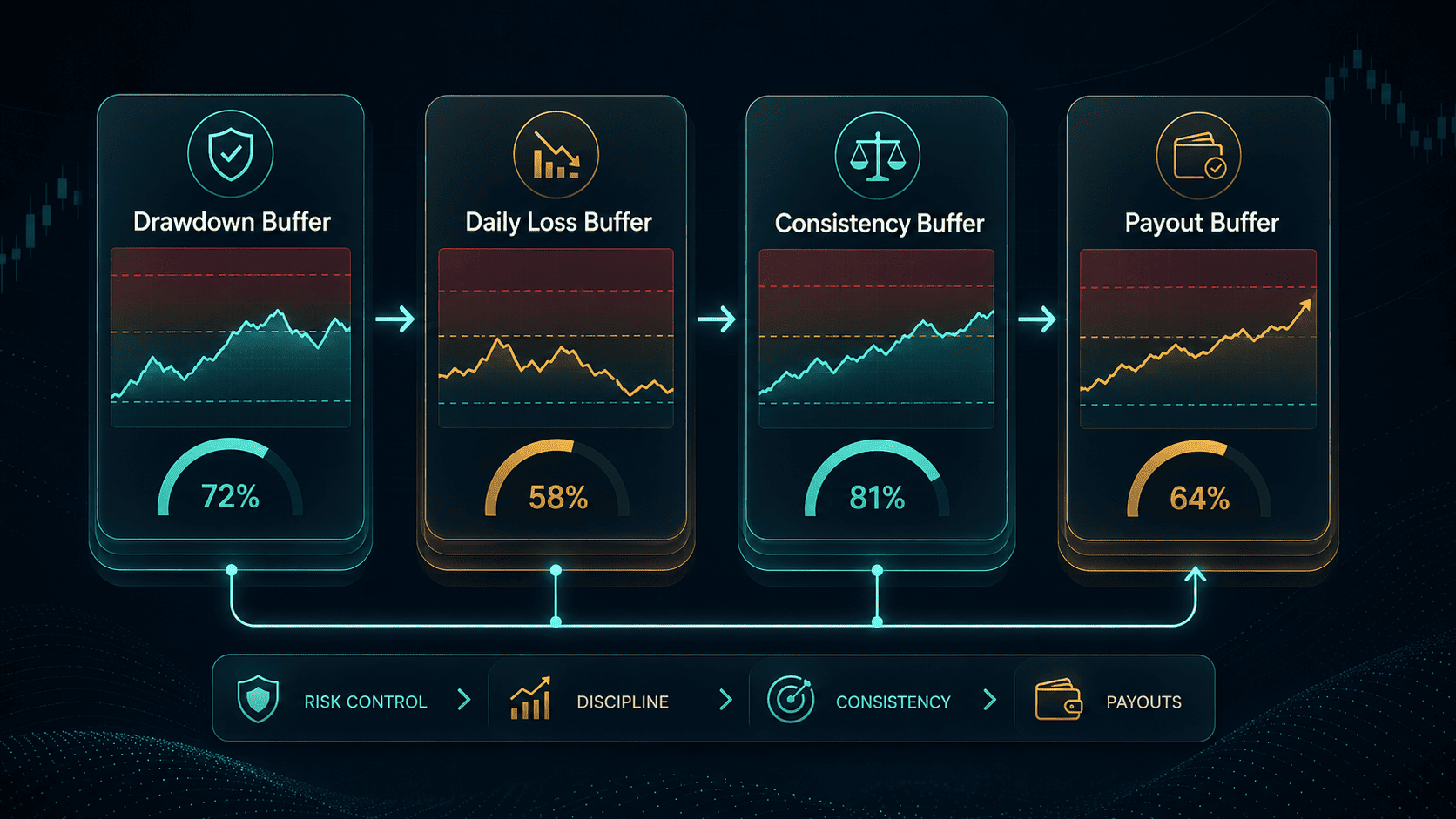

Buffer Rules: The Account Needs Room Before It Needs Speed

Buffer rules decide how much room the account has between current equity or balance and the next rule boundary. The trader’s job is to protect that room. Without buffer, every normal futures rotation becomes a threat.

Track four buffers at the same time. The mistake is tracking only the maximum-loss number.

| Buffer type | Question to answer | Futures-specific risk | Action before the next trade |

|---|---|---|---|

| Drawdown buffer | How far is current equity from the account-level loss floor? | One fast futures rotation can consume more of the lifecycle room than expected | Resize when the account is damaged; do not increase size because the target feels farther away |

| Daily loss buffer | How much room remains before the daily stop or firm daily limit? | Cash open, news and fast liquidity changes can create poor fills or larger-than-planned losses | Block the next trade if the full stop plus cost cushion would put the account too close to the limit |

| Consistency buffer | Is the best day or top-two-day result becoming too large? | One strong futures session can dominate total account profit | Set a daily profit stop and reduce size after a large winning day |

| Payout or review buffer | Will the account remain eligible and usable after review or withdrawal? | The trader may keep trading after the account is already pass-ready, creating avoidable review risk | Stop when the target, rule state and next-stage conditions are clean |

Daily Reset Example

A futures trader is safe before the reset only if the account remains safe after the reset formula is applied. If the new day recalculates from balance, equity or a trailing floor, the trader must recalculate the buffer before holding or adding exposure.

| Account moment | Example account state | Risk-management decision |

|---|---|---|

| Before reset | Account has realised profit but one open futures position is moving quickly | Do not assume the next day gives more room until the rule calculation is known |

| At reset | The firm may use a new balance, equity, end-of-day value or trailing reference | Update the daily loss floor and maximum-loss floor in the journal |

| After reset | The same open position can now sit closer to the new daily floor | Reduce, close or skip new trades if the next stop no longer fits |

For the detailed account-boundary explanation, read daily, maximum and trailing drawdown rules. For the reset-clock problem, read daily loss reset time. For the dedicated concentration formula, read the prop firm consistency rule.

Consistency: why one strong futures session can slow the pass

Consistency rules punish profit concentration. In futures challenges, this usually matters because one strong session can produce a large share of the target. The account may be profitable, but the pass can still become harder.

This is not about trading timidly. It is about avoiding a profit shape that forces extra trading at the worst possible moment.

Imagine the account is close to passing after one large NQ move. Emotionally, the trader feels almost done. Rule-wise, the account may now have a best-day problem. The trader must keep trading to distribute the profit more evenly.

That extra trading is dangerous. The trader is no longer taking trades because the market is clean. They are taking trades because the account needs a better-looking profit curve.

Set a daily profit stop as well as a daily loss stop

Most traders understand a daily loss stop. Fewer set a daily profit stop. In a futures challenge, that is a mistake.

A daily profit stop protects two things. First, it stops the trader from giving back a good session. Second, it prevents one day from becoming too dominant. The account needs distributed profit, not one heroic spike.

After a strong day, reduce size the next session. Do not use confidence as a sizing model. Confidence has a bad track record near targets.

The risk plan: size from the stop, not from the target

A futures prop firm risk plan must start with the stop distance and contract size. The target does not decide size. The breach line does.

Before entering a trade, the trader should already know the loss in account currency if the stop is hit. If that number is uncomfortable, the position is too large or the stop is wrong.

Use a three-layer risk ladder

A clean futures challenge plan can be built as a risk ladder:

- Base size: used at the start of the challenge or after a losing day.

- Buffer size: used only after realised profit creates enough room.

- Protective size: used near the profit target or after a large winning day.

The base size should be boring. That is the point. It lets the trader collect information without putting the account under stress.

Buffer size is not a licence to gamble. It is a controlled increase after the account has earned room. Protective size is used near the target, because the cost of giving back progress is higher than the benefit of finishing one session earlier.

For a separate risk budget framework, read risk management strategy for prop challenges.

Do not trade every futures session the same way

The Asian session, European morning, US cash open and late US session do not behave the same way. A fixed contract size across every session ignores volatility.

The US cash open may offer opportunity, but it can also produce fast fills, wider rotations and emotional decisions. Midday can be cleaner for some traders but dead for others. Late-day futures movement can be sharp because positions are being adjusted into the close.

The challenge plan should name the sessions you are allowed to trade. It should also name the sessions you are not allowed to revenge-trade. Vague freedom is where bad futures accounts go to die.

Challenge Phase Plan: Protect First, Build Second, Stop Cleanly

A futures prop firm challenge needs phases. The account should not be traded the same way on Day 1, after buffer is built, after a loss, near the target or after passing.

The worst mistake is increasing aggression near the target. That is the moment to reduce avoidable risk.

| Challenge phase | Main goal | Contract behaviour | What to recalculate | Failure path to avoid |

|---|---|---|---|---|

| Start of challenge | Confirm execution quality and protect the starting buffer | Use the smallest size that still makes the setup meaningful | Daily loss floor, max-loss floor, tick risk and personal stop | Oversizing because the account feels fresh |

| After early profit | Build realised cushion without creating a best-day problem | Add size only if stop distance still fits the risk plan | Best-day concentration, give-back limit and remaining drawdown room | Turning confidence into a larger contract count |

| After a losing day | Stop the account entering recovery mode | Return to base size or stop trading for the session | Remaining daily loss room and behaviour triggers | Trying to make the loss back before the session ends |

| Near the target | Finish cleanly and avoid giving back pass-ready profit | Reduce size, take only high-quality setups and avoid forced trades | Target, valid-day status, consistency profile and review buffer | Taking one more futures trade because the target is close |

| After passing | Prepare for the next account stage, verification and payout review | Do not assume the next stage has the same risk room | Funded-stage rules, KYC, payout process and account-state requirements | Continuing to trade before understanding the next-stage conditions |

After the account appears pass-ready, read what happens after you pass a prop firm challenge before changing the account state.

Execution checklist before the first futures trade

The pre-trade checklist should remove decisions from the live moment. If the trader has to calculate contract risk while price is moving, the plan is too loose.

Before the first futures trade of the challenge, write down the following items:

- The account breach line and current buffer.

- The personal daily stop.

- The maximum loss allowed on one trade.

- The exact contracts allowed for each instrument.

- The session window where trading is allowed.

- The daily profit level where trading stops.

- The rule for reducing size after a losing day.

- The rule for stopping once the account is pass-ready.

This is the practical side of a prop firm challenge checklist. It is not paperwork. It is account protection.

Common mistakes that fail futures prop firm challenges

Most futures challenge failures are not caused by one bad read of the market. They come from a bad account path. The trader lets size, correlation or target pressure distort the next decision.

The common mistakes are easy to name and hard to stop in real time:

- Using mini contracts before the account has earned buffer.

- Trading NQ with the same risk assumptions used for slower instruments.

- Counting correlated index trades as diversification.

- Moving stops wider because the account is close to the target.

- Ignoring the best-day percentage after a large session.

- Continuing to trade after the account is already pass-ready.

The last mistake is brutal. Traders often fail because they keep trading after the job is done. They want a cleaner number, a bigger cushion or a faster funded transition. That extra trade can erase the pass.

For what happens after a successful evaluation, read what happens after you pass a prop firm challenge. The funded stage has its own rules, and the risk plan should change before the first funded trade.

Alpha Insight: futures challenges are buffer conversion tests

A futures prop firm challenge is not mainly a strategy test. It is a buffer conversion test.

The trader starts with limited risk space. Every trade either converts part of that space into realised profit or consumes it. The job is to convert enough buffer into profit target progress without letting one session dominate the account or one pullback reach the breach line.

This is why “easy strategy” claims are dangerous. A clean setup can still fail the account if the stop is too wide, the contract size is too large or the profit arrives in the wrong shape.

The market can be right and the account can still be wrong. That is the futures challenge problem.

Using AIFO Rules as the Final Account Check

Last checked on : AIFO’s public platform page describes MT5 trading for forex, indices, commodities and more. This article should therefore not be read as an AIFO futures-contract availability page. Use it as an educational guide for futures-style contract risk, then verify the actual product, symbol specification and account rules inside the platform and official AIFO documentation.

| AIFO check | What to verify before applying this guide | Why it matters | Official reference |

|---|---|---|---|

| Product and symbol type | Whether the instrument is an exchange-traded futures contract, an index/commodity CFD, or another MT5 symbol | Tick value, contract size, margin, fees and session behaviour may not match a futures example | AIFO trading platform |

| Daily loss and maximum loss | The current account floor, calculation base, reset reference and dashboard values | The same trade risk can be safe on one account path and too large on another | AIFO trading rules |

| Consistency and payout gate | Whether the account has a best-day, top-two-day or payout-review concentration rule | A strong session can create review risk even when the account is profitable | AIFO trading rules |

| Execution and tools | Manual trading, EA, copier, holding, news, VPS/VPN and restricted-activity rules | Platform acceptance does not automatically mean the behaviour survives review | AIFO trading rules |

| Payout path | Whether the account is eligible for review, verification and withdrawal after the challenge stage | Passing the target is not the same as approved payout readiness | AIFO payout process |

The trader who passes cleanly is not the trader who extracts the most from every session. It is the trader who leaves enough room for the next session and the next account stage.

Verification note: Save the symbol specification, account model, rule version, dashboard values and date checked before using any futures contract example inside an AIFO account.

FAQ

The best way is to size positions from the loss line backwards. Convert every trade into stop distance, tick value and contract count, then check whether the risk fits the daily loss room, maximum-loss room, consistency profile and pass-ready state. Do not start from the number of contracts needed to reach the target quickly.

Micro contracts are often cleaner during the early challenge phase because they allow finer risk control. Minis may be useful after realised buffer exists, but using them too early can make normal futures movement too large for the account. Contract choice should follow stop distance, tick value, current drawdown room and the account’s loss rules.

Use this formula: stop distance in ticks × tick value × number of contracts. Then compare the result with the allowed money risk from the failure-buffer calculation. Always verify the actual contract specification, commission, fees and platform symbol details before placing the order.

Consistency matters because one large futures session can dominate the account’s total profit. Some firms may then require more profit, more trading days or a cleaner distribution before the account qualifies. A daily profit stop helps protect the account from creating a best-day problem.

One trade a day can be enough if the setup quality, stop distance, contract size and trading-day rules fit the account. The danger is assuming fewer trades automatically means lower risk. One oversized trade can be more dangerous than several smaller trades with defined stops and controlled exposure.

Reduce size and protect the pass-ready state. Avoid adding trades just to finish faster. Check the consistency profile, current buffer, valid-day requirements and next-stage rules before taking another position. Many traders fail because they keep trading after the account is already clean enough to move forward.

No. This is an educational guide for futures-style contract risk. AIFO traders should verify the actual MT5 product, symbol specification, account model and live rules before using any futures example. Use the AIFO trading platform page and AIFO trading rules as current account references.