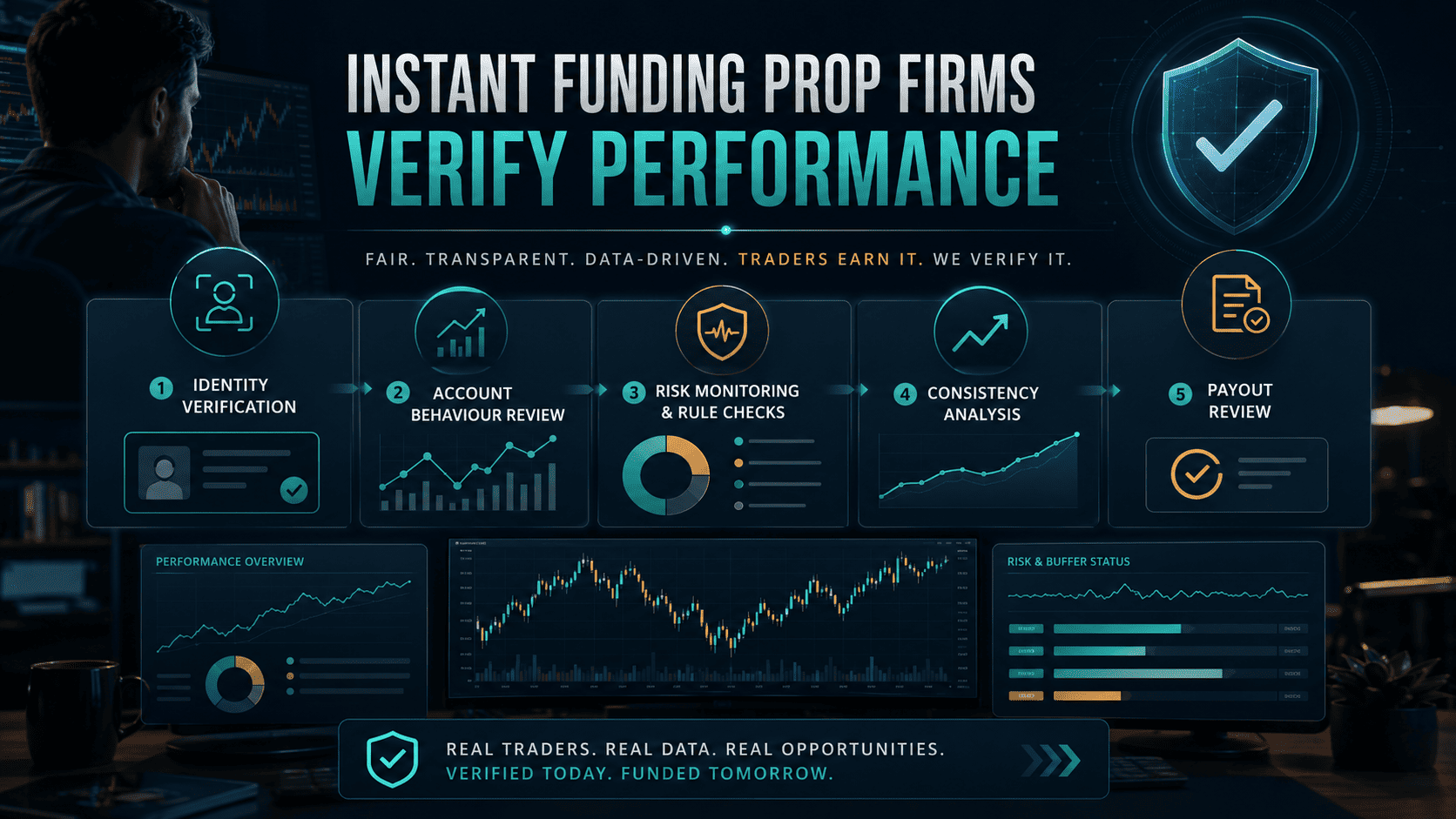

Instant funding prop firms verify trader performance after access by reviewing account behaviour, risk control, consistency, trading conduct, identity and payout eligibility. Fast account access does not mean the firm has accepted every future profit as payable. It means the account starts under rules immediately, and the trader’s performance is judged through the path from first trade to payout request.

This article is the performance-verification child guide inside the AIFO Instant Funding program cluster. Use the product page for the account route, and use this page to understand what gets checked after access: identity, account ownership, drawdown behaviour, trade history, consistency, prohibited strategies and payout review.

The phrase “instant funding” can make the process sound lighter than it is. The account may open faster, but the review does not disappear. It moves deeper into the trading path.

Instant Funding Verification: Access First, Proof Later

| Verification stage | When it happens | What the firm checks | Why traders misunderstand it |

|---|---|---|---|

| Account access | After purchase or activation of the instant route | Account model, rule acceptance, dashboard setup and trading permissions | Fast access is mistaken for a completed performance review |

| Live account monitoring | From the first order onward | Daily loss, maximum loss, position size, trade duration, exposure and account path | Traders look only at final profit instead of the route that created it |

| Behaviour review | During trading or when unusual patterns appear | Copying, account sharing, EAs, HFT, latency, news behaviour and restricted strategy signals | Platform acceptance is mistaken for rule approval |

| Consistency review | Before payout or during account review | Best-day concentration, top-two-day concentration and profit distribution | One strong day is treated as proof of skill instead of review risk |

| Payout review | When the trader requests withdrawal | KYC, account status, eligible profit, open positions, payout buffer, payment destination and rule history | Dashboard profit is mistaken for approved cash |

The clean way to read instant funding is simple: access is faster, but proof is delayed. The trader is being verified through account behaviour, not only through a pass target.

The First Check Is Identity and Account Ownership

The first verification layer is not trading skill. It is identity and account ownership. The firm needs to know that the person trading, receiving payouts and passing review is the actual account owner.

| Ownership check | What is verified | Why it affects performance review | Risk if unclear |

|---|---|---|---|

| Legal identity | ID document, name, date of birth and profile details | The firm needs to link the account history to one verified trader | Payout can be delayed or blocked during KYC review |

| Liveness or selfie check | The person verifying matches the account owner | Prevents proxy verification and account transfer | The account may be flagged as third-party controlled |

| Payment destination | Bank, card, wallet or provider details belong to the permitted recipient | Performance proof is incomplete if the payout recipient does not match the trader | Withdrawal can be returned, reviewed or rejected |

| Device and access pattern | Whether the same trader appears to control the account | Shared devices, unusual IP patterns or unexplained access can weaken account independence | The firm may review account sharing or third-party management |

| Trade source | Whether decisions came from the account owner | Copied signals or group execution can make performance less attributable to the trader | Profit may be treated as signal copying, coordination or restricted behaviour |

For AIFO, review the AIFO KYC verification process before reaching payout pressure. Fast access does not make an instant account portable, transferable or safe for shared trading.

The Real Performance Check Is the Account Path

Instant funding prop firms verify trader performance by reading the account path, not just the final profit number. The review asks how the account moved from starting balance to payout request.

A smooth profit path and a reckless profit path can end at the same balance. They do not carry the same risk.

| Account-path signal | What the firm may review | Clean performance signal | Review-risk signal |

|---|---|---|---|

| Equity path | Floating P&L, intraday dips, reset behaviour and recovery path | Profit was made while preserving buffer | Profit came after repeatedly sitting near breach lines |

| Daily loss behaviour | How close the account came to the daily floor | Trader stopped before hard limits were threatened | Trader used most of the daily limit and recovered late |

| Maximum loss room | Account-level drawdown, lifecycle floor and equity highs | Position size stayed inside the real failure buffer | Trader sized from headline balance instead of loss room |

| Position size | Risk per trade, scaling after wins or losses and correlated exposure | Risk stayed stable and explainable | Size increased after losses or near payout pressure |

| Open-position state | Exposure during review, payout request, reset, news or weekend | Account state was clean before review or payout request | Open trades or pending orders created avoidable payout friction |

| Dashboard and platform data | Official dashboard values, MT5 values, timestamps and account status | Trader can explain account metrics from the official dashboard | Trader relies on local interpretation while firm metrics show a different state |

If a trader’s MT5 balance and dashboard data do not match, that difference can affect their own reading of account status. The AIFO page on AIFO dashboard balance mismatch is useful because verification often depends on the firm’s official account metrics, not the trader’s local interpretation.

For AIFO-specific account rules, read the live AIFO trading rules before placing the first trade. Verification starts when trading starts, not when payout is requested.

Consistency and Behaviour Review Decide Whether Profit Is Clean

Consistency checks verify the shape of profit. Behaviour review verifies the method that created it. Instant funding needs both because there may be no long evaluation phase before account access.

| Review area | What is checked | Why it matters | Trader control |

|---|---|---|---|

| Single-day concentration | Whether one day creates too much of total account profit | One strong day can make profit look less repeatable | Set a daily profit cap before the account reaches review |

| Top-two-day concentration | Whether two days dominate the payout period | Several fast wins can still create payout-readiness pressure | Track profit distribution before adding more risk |

| Trade-size concentration | Whether one oversized trade carries most of the result | The firm may read it as event risk instead of repeatable skill | Keep position size stable and within the written risk plan |

| Restricted automation | Expert Advisors, bots, copy tools or automated execution | Platform acceptance does not mean the method is allowed | Use only methods the rulebook explicitly permits |

| Copying and coordination | Mirrored trades, group entries, related accounts, shared devices or signal use | The account may no longer prove independent trader performance | Trade your own account, from your own decision flow |

| Execution abuse | Latency, arbitrage, platform glitch exploitation, HFT or toxic-flow patterns | Profit can be visible and still fail conduct review | Avoid strategies built on loopholes or technical exploitation |

Traders should read AIFO consistency score and AIFO restricted trading before using automation, signals, trade copiers or shared strategy groups. A strategy that looks harmless on a personal retail account can become a violation inside a funded model.

A better plan is to control profit shape from the beginning. Set a daily profit stop. Reduce size after a large day. Avoid turning one strong session into a payout problem.

Payout Review Is the Final Performance Audit

Payout review is where instant funding verification becomes real. The trader has profit. Now the firm checks whether that profit can be paid under the rules.

This is not just a payment step. It is an account audit.

| Payout review lane | What may be checked | Why a profitable account can still fail | What to prepare before requesting |

|---|---|---|---|

| KYC and account ownership | Identity, account holder, payment recipient and payout destination | The trading record does not match a clean verified owner | Complete verification and use matching payment details |

| Account state | Daily loss history, maximum loss history, open positions, pending orders and account status | The account is profitable but not payout-ready | Save the clean account state before submitting |

| Consistency | Best-day, top-two-day, largest trade and profit distribution | Profit exists but is too concentrated for the payout rules | Calculate the relevant ratio before requesting payout |

| Trading conduct | Restricted strategies, copy patterns, EAs, HFT, news behaviour and account access | Profit was created through a method that the firm does not permit | Keep a rule-compliant trade history and support evidence |

| Payout buffer | Amount requested, retained buffer and post-withdrawal account safety | The request would leave the account too fragile or close the account under full-withdrawal rules | Calculate payout-available profit before submitting |

| Payment settlement | Approved payout amount, payment method, processing route and final arrival | Approval and settlement are not the same moment | Track request status, approval status and final receipt separately |

Before submitting a withdrawal, traders should read the AIFO payout process and instant funding payout rules. The trader should know what is being reviewed before the request is made, not after a delay starts.

If a review leads to a restriction or termination, the trader should understand the AIFO violation policy. The better move is to avoid review problems before they appear.

How Traders Should Prepare Before the First Trade

The trader should prepare for verification before placing the first order. Waiting until payout is too late. Every trade should be planned as something that may later be reviewed.

| Preparation step | What to do before trading | Why it protects payout review | Related guide |

|---|---|---|---|

| Choose the exact account route | Compare Instant with 1-Step, 2-Step, 3-Step and other account models | Rules can differ by account path | AIFO account models |

| Write the risk map | Record daily loss, maximum loss, single-trade risk, consistency and payout buffer | Review starts with account-state compliance | Instant funding drawdown rules |

| Build a personal stop plan | Set a daily stop below the firm limit and a rule for stopping after behaviour breaks | Prevents near-breach recovery patterns | Risk management strategy |

| Control profit shape | Use a best-day cap and reduce size after unusually strong sessions | Prevents one day from dominating payout review | Consistency rule |

| Avoid restricted methods | Do not rely on copy trading, account sharing, EAs, latency, HFT or loopholes unless expressly permitted | Prevents profitable but non-compliant trade history | Prop firm challenge rules |

| Prepare KYC and payout evidence | Use your own documents, own account and matching payout destination | Reduces identity and payment friction at the payout stage | First payout rules |

Alpha Insight: Instant Funding Is Delayed Proof

Instant funding prop firms do not verify promises. They verify account behaviour.

The firm does not need to know on Day 0 that the trader is skilled. It needs rules that limit downside and a review process that filters the account path before money leaves the system.

That is the business logic behind instant funding. The trader receives faster access. The firm receives more account data. The payout review decides whether that data proves clean performance.

A trader who understands this will not treat instant funding as a shortcut. They will treat it as a faster entry into a stricter audit trail.

Using AIFO as the Final Rule Check

Last checked on : AIFO Instant currently presents no traditional evaluation phase, 2% Daily Drawdown, 2% single-trade floating loss, 5% Maximum Loss for Standard, 4% Maximum Loss for Elite / No Commission, 15% single-day concentration, 25% top-two-day concentration and payout on demand under the public Instant and Rules pages.

| AIFO verification item | Current public rule or process | How it verifies performance | Official reference |

|---|---|---|---|

| Account access | No traditional evaluation | Performance is reviewed through account behaviour after access | AIFO Instant Funding |

| Drawdown and floating-loss rules | 2% Daily Drawdown, account-specific Maximum Loss and 2% single-trade floating loss | Shows whether the trader controls risk from the first trade | AIFO trading rules |

| Consistency | 15% single-day concentration and below 25% top-two-day concentration under current public Instant rules | Checks whether profit distribution is repeatable enough for payout readiness | AIFO trading rules |

| Execution conduct | Manual trading; Expert Advisors and automated systems are not allowed | Separates manual trader performance from tool-led or prohibited methods | AIFO EA FAQ |

| Payout process | Eligibility, review, approval and settlement are separate stages | Turns profitable account history into a final payout audit | AIFO payout process |

The account is being verified from the start. The safest trader is not the one who explains the trade best after review. It is the one whose account history does not need much explanation.

Related Guides for Instant Funding Verification

- Instant funding drawdown rules — daily loss, maximum loss, single-trade floating loss and payout buffer.

- Instant funding payout rules — first withdrawal, KYC, buffer, review and payout-on-demand conditions.

- Why prop firm payouts get denied — rule, identity, payment and review problems that block payout.

- Prop firm challenge rules — daily loss, consistency, conduct and rule-stack checks.

- Best instant funding prop firms — commercial comparison after the verification framework is understood.

FAQ

They verify performance by reviewing account behaviour after access: identity, account ownership, drawdown path, trade history, position size, consistency, prohibited strategies, open-position state and payout eligibility. The final profit number is not enough; the firm checks how the profit was made.

Some signup, payment or identity checks can happen before access, but the main performance verification usually happens after account access. Instant funding gives faster entry into a rule-bound account. The trader still has to prove performance through trading behaviour and payout readiness.

No. KYC verifies identity, account ownership and payout-recipient details. Performance verification checks the account path, trading behaviour, drawdown control, consistency, restricted methods and payout eligibility. Both matter, but they answer different questions.

AIFO’s current public Instant rules include Daily Drawdown, Maximum Loss, single-trade floating loss, consistency, manual trading requirements and payout-on-demand conditions. Traders should check the live AIFO Instant Funding, AIFO trading rules and payout process before trading.

A profitable account can fail payout review if the profit came from a rule breach, prohibited strategy, excessive best-day concentration, failed KYC, mismatched payout details, open trades during review or an account state that does not meet payout conditions. Profit has to be eligible before it can be paid.

Firms usually check drawdown behaviour, position size, trade duration, copied patterns, unusual account links, high-risk recovery behaviour, one-day profit concentration and signs of prohibited methods such as unrelated copy trading, reverse trading, account sharing, HFT, latency abuse or platform exploitation.

Traders should read the rules before trading, keep a personal daily stop, avoid restricted strategies, track best-day profit, use their own account and identity documents, and check payout eligibility before requesting withdrawal. The goal is to keep the account history clean enough that payout review needs little explanation.